Family Banking: The Power of the Win-Win-Win

Families already trust their financial institution with the big things. But when it comes to teens, allowances, and everyday money moments, many are quietly building habits somewhere else. This article explores how family banking helps institutions stay part of daily family life, creating a win for parents, teens, and long-term generational growth.

The Real Competition in Teen Banking Is Daily Habit, Not Other Banks

Parents already trust their bank with the big stuff, their mortgage, their savings, and their long-term goals.

But when it's time for a teenager to get a first debit card, a quiet shift happens. Instead of expanding their relationship with you, manyfamilies quietly take that next step somewhere else.

It’s not because they stopped trusting you. It’s simplybecause they had an immediate problem to solve, and someone else solved itfaster.

So, parents turn to the apps their kids ask for: Greenlight,Venmo, or Cash App.

What starts as a simple way to handle allowances, chores, or lunch money quickly becomes something much bigger. Over time, that single app captures:

• Early money habits

• Brand familiarity

• Real trust

• Future loyalty

Every time a parent opens that competitor's app to send money, they are stepping into someone else’s world. They see someone else’s notifications, someone else’s offers, and someone else’s vision for their child's future financial life.

The Shift in Banking Digital Strategy

Most traditional financial institutions still think in terms of individual products. But fintechs understand something deeper: daily habits create lifelong relationships.

Fintechs don't win families over with better interest rates; they win them by becoming a daily utility.

Every time a teenager checks their balance after school or a parent sends money for chores, a habit is being formed. Once those daily habits take root somewhere else, the core financial relationship naturally follows.

The real danger here isn't a lost debit card balance, it's that your institution becomes invisible simply because you aren't in the palm of their hand every day.

To stay visible, institutions have to stop offering isolated products and start offering ecosystem solutions.

Family Banking as a Financial Institution Growth Strategy

This is the exact problem family banking solutions are designed to address.

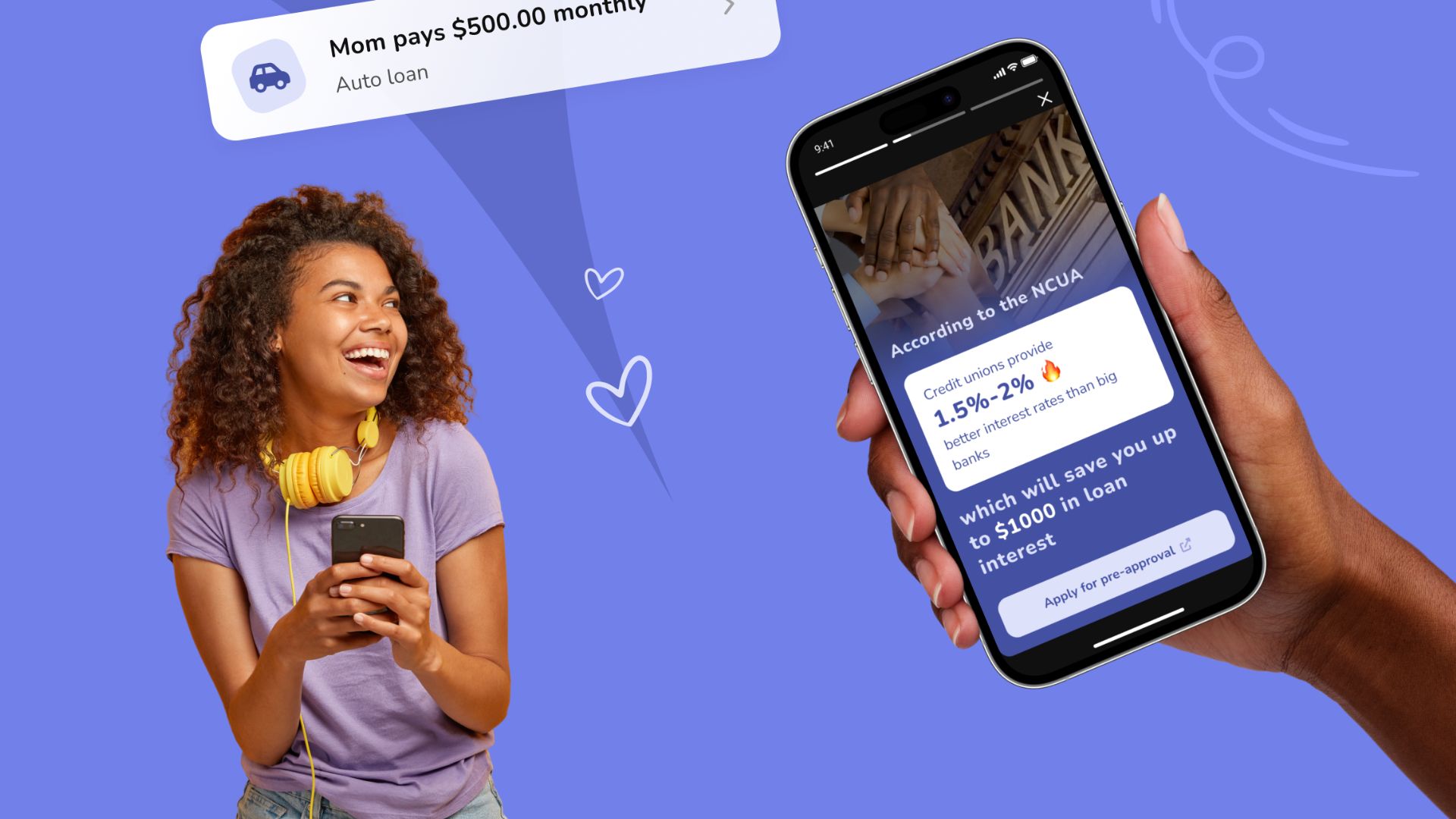

For example, platforms like Boucoup help financial institutions extend their relationship into the daily financial lives of families, so parents and teens can manage allowances, spending, and financial learning inside the same trusted banking relationship.

Instead of pushing families to external apps for teen banking, these solutions keep those interactions inside the financial institution.

This shift isn't about expanding a product catalog. It's about maintaining relevance where it counts most, within the family’s daily financial ecosystem.

A Win-Win-Win in Family Banking

A family banking solution works because it aligns incentives across everyone in the relationship.

Parents, teens, and financial institutions are not competing for different outcomes.

Each one wins in their own way.

The win of Parents - Less Anxiety, More Peace of Mind

Parents don’t want to choose between convenience and trusted values.

They want modern tools inside the financial relationship they already trust.

The real driver is not technology. It is anxiety.

They worry their kids will enter adulthood financially nunprepared, without confidence, habits, or guidance.

Family banking helps reduce that anxiety early.

The Win for Teens: Confidence Instead of Mistakes

Most teenagers are expected to magically understand money the day they turn 18, without ever being given a map.

Most teens are expected to understand money long before they are ever taught how it works.

A better first financial experience changes that trajectory.

Instead of fear, teens build confidence.

Instead of confusion, they build habits.

Instead of reacting later, they learn early.

The goal is not a debit card. It is financial confidence before adulthood.

The Win for Financial Institutions: Building an Organic Growth Engine

For financial institutions, family banking is not a youth product.

It is a long-term digital strategy.

By keeping family financial activity inside the institution, credit unions secure:

• daily engagement

• protected deposits

• stronger retention

• early trust formation

• future lending relationships

The institution that wins the first financial experience often wins the long-term relationship.

The Future of Family Banking

Traditional banking was built on trust, safety, and helping people build better financial lives.

That mission still matters.

But families don’t experience banking as products, they experience it through daily financial habits.

Allowance. Spending. Saving. First jobs. First purchases.

The institutions that stay present in those small, everyday family moments are the ones that stay part of the long-term relationship.

Because the future of family banking won’t be defined by products or pricing, it will be defined by who becomes part of the daily financial habits of families.

Welcome to our blog on all things BankingON and our perspective on what's going on in the Credit Union and Banking Industry. If you get a chance, share our posts on social media!

Featured Posts